Introduction & Market Context

Trane Technologies plc (NYSE:TT) delivered first-quarter 2026 results that exceeded Wall Street expectations on April 30, 2026, driven by exceptional demand in commercial HVAC markets and record bookings that position the company for sustained growth. The climate solutions provider reported adjusted earnings per share of $2.63, beating analyst forecasts of $2.53 by 3.95%, while revenue of $4.97 billion surpassed expectations by 3.33%.

The company’s stock responded positively to the results and raised full-year guidance, climbing 4.35% in pre-market trading to $485.20, approaching its 52-week high of $501.69. With a market capitalization of $110.6 billion and a P/E ratio of 37.74, Trane Technologies trades at a premium valuation that reflects investor confidence in its growth trajectory, though InvestingPro analysis suggests the stock appears overvalued relative to fundamentals.

Quarterly Performance Highlights

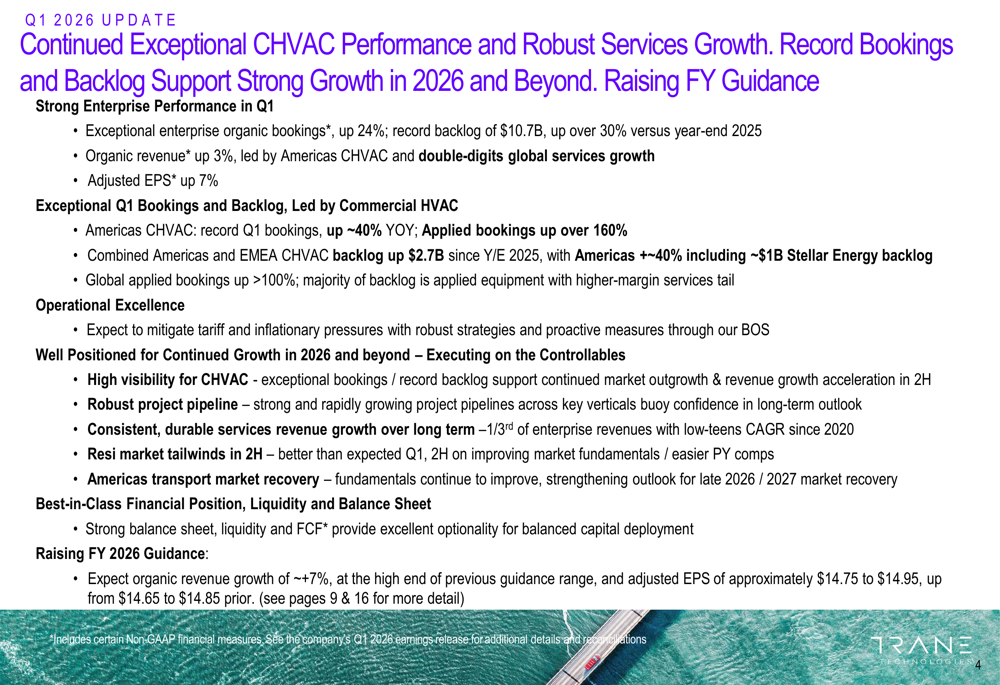

The company’s Q1 2026 presentation revealed a strong operational performance underpinned by record-breaking bookings and backlog growth. As detailed in the following performance overview, Trane Technologies achieved enterprise organic bookings growth of 24% year-over-year, with particularly exceptional strength in the Americas commercial HVAC segment.

The company’s record backlog reached $10.7 billion, representing a 30% increase from year-end 2025 and providing substantial revenue visibility for 2026 and beyond. Americas commercial HVAC bookings surged approximately 40% year-over-year, with applied equipment bookings skyrocketing more than 160%. This exceptional demand was driven by continued strength in data centers and core markets including higher education, government, and healthcare facilities.

Organic revenue growth of 3% year-over-year reflected a mix of flat equipment sales offset by strong low-double-digit services growth. Services now represent approximately one-third of enterprise revenues and have grown at a low-teens compound annual growth rate since 2020, providing a consistent and durable revenue stream.

Detailed Financial Analysis

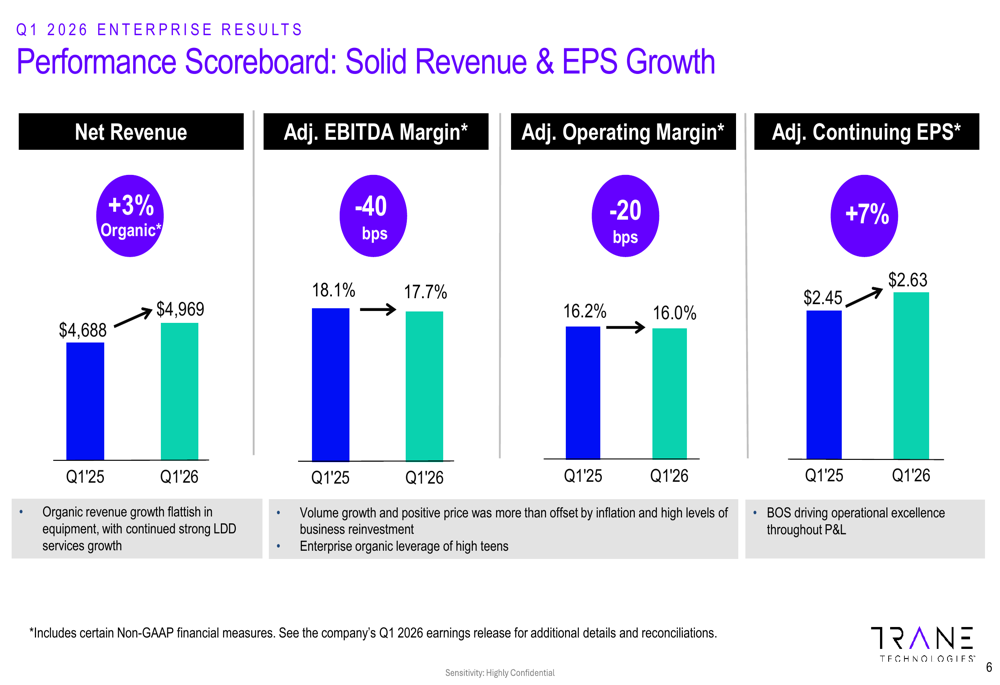

The following charts illustrate the company’s solid revenue and earnings per share growth, though margin compression presented challenges in the quarter.

While revenue and EPS grew year-over-year, adjusted EBITDA margin contracted 40 basis points to 17.7% from 18.1% in the prior-year period, and adjusted operating margin declined 20 basis points to 16.0%. Management attributed the margin pressure to inflation, high business reinvestment, and integration costs, which offset volume growth and positive pricing. However, the company’s Business Operating System (BOS) drove operational excellence throughout the P&L, enabling 7% adjusted EPS growth despite the margin headwinds.

Enterprise organic leverage remained strong in the high-teens range, demonstrating the company’s ability to convert revenue growth into earnings even amid cost pressures. The company emphasized its acceleration of incremental business reinvestment across all segments to pull forward high-ROI innovation and growth initiatives.

Segment Performance Analysis

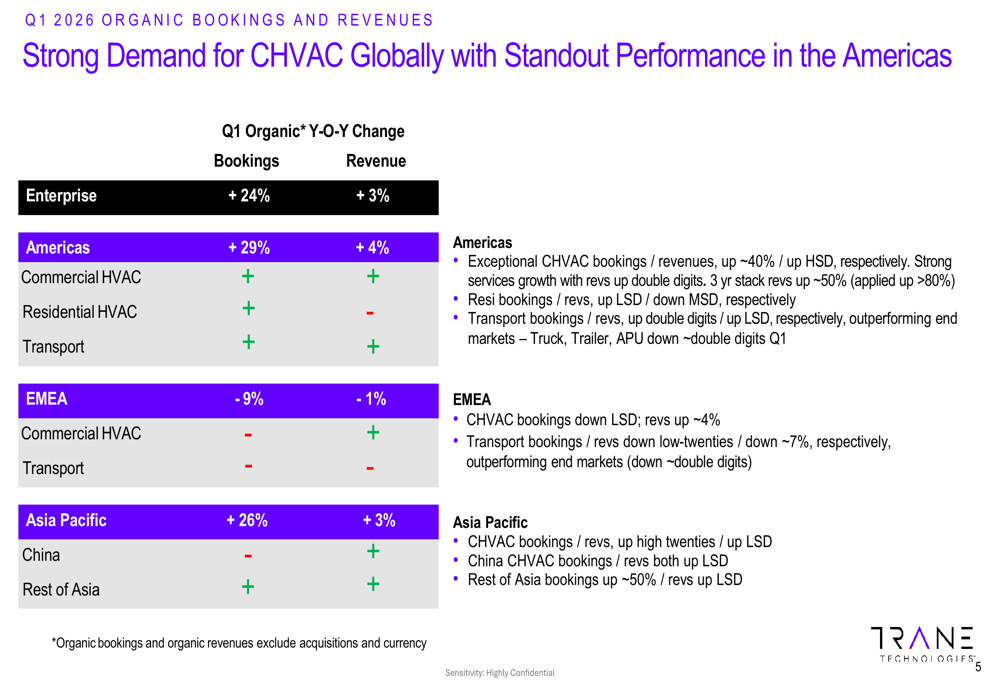

Regional performance varied significantly across Trane Technologies’ three geographic segments, as shown in the following breakdown of bookings and revenues.

The Americas segment delivered exceptional performance with bookings up 29% and revenue up 4% organically. Commercial HVAC bookings and revenues increased approximately 40% and high-single-digits respectively, while services revenue grew at double-digit rates. The residential HVAC business showed mixed results with bookings up low-single-digits but revenues down mid-single-digits. Transport bookings and revenues grew double-digits and low-single-digits respectively, significantly outperforming end markets where truck, trailer, and APU markets declined approximately double-digits.

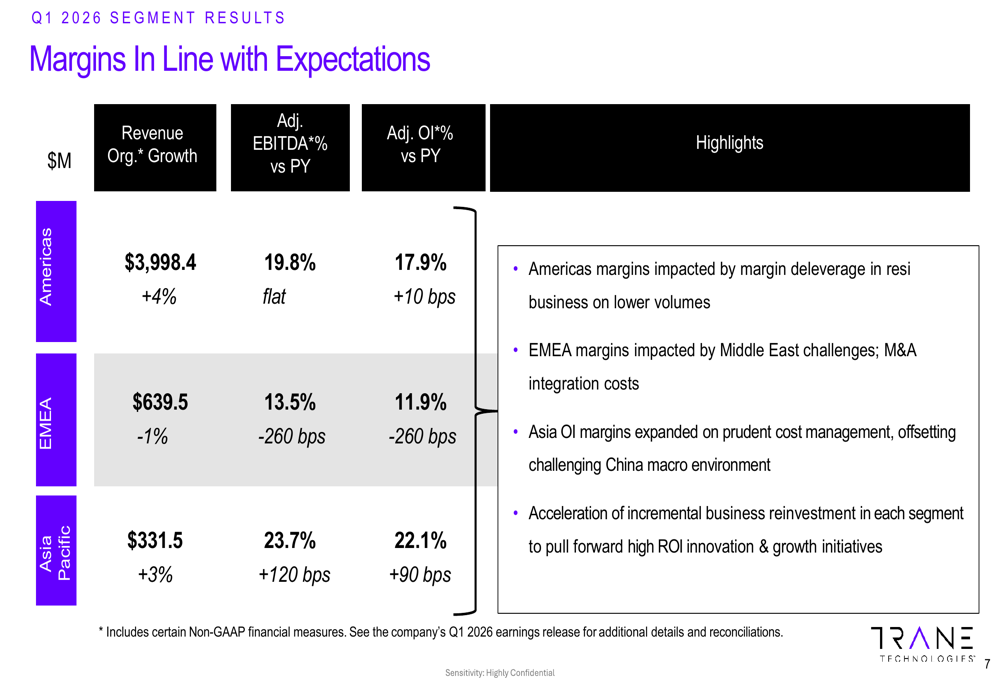

The following segment margin analysis reveals the operational dynamics across regions.

Americas segment margins remained relatively stable with adjusted EBITDA flat at 19.8% and adjusted operating income up 10 basis points to 17.9%, despite margin deleverage in the residential business due to lower volumes. EMEA faced more significant challenges, with adjusted EBITDA and operating margins both declining 260 basis points to 13.5% and 11.9% respectively, impacted by Middle East headwinds of approximately $25 million in revenue and $0.02 in EPS, along with M&A integration costs. Asia Pacific demonstrated strong margin expansion with adjusted operating income margin up 90 basis points to 22.1%, driven by prudent cost management that offset a challenging China macroeconomic environment.

Strategic Initiatives & Growth Drivers

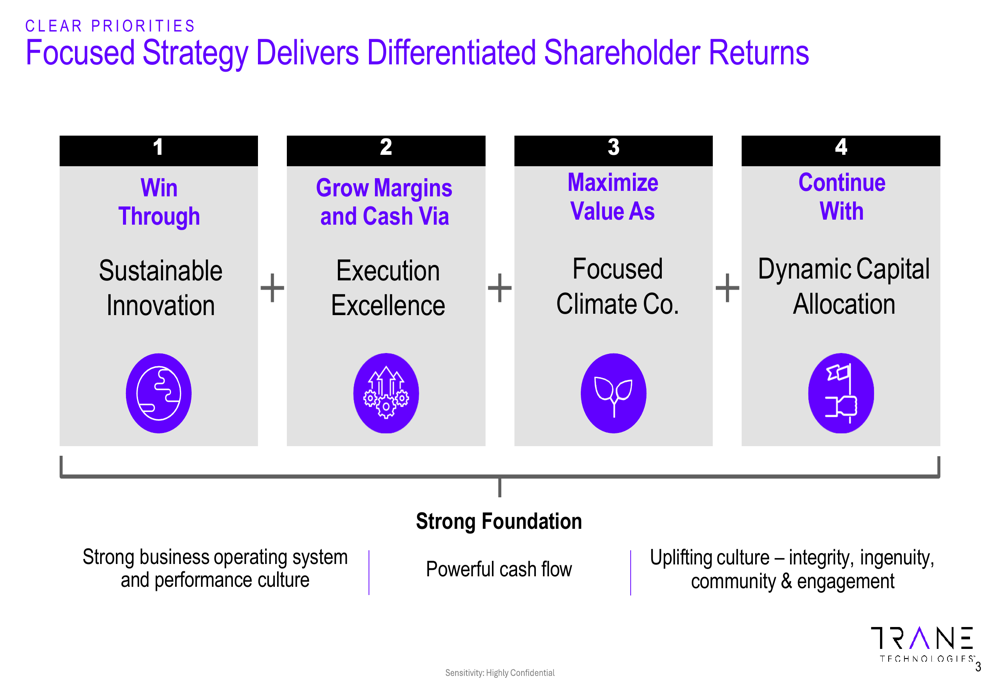

Trane Technologies’ strategic framework centers on four key pillars designed to deliver differentiated shareholder returns, as illustrated in the company’s focused strategy overview.

The company’s strategy emphasizes winning through sustainable innovation, growing margins and cash via execution excellence, maximizing value as a focused climate company, and continuing dynamic capital allocation. This approach is supported by a strong business operating system, powerful cash flow generation, and an uplifting culture characterized by integrity, ingenuity, and community engagement.

Data center cooling emerged as a particularly significant growth driver in Q1 2026. The company’s acquisition of Stellar Energy, which closed earlier in the year, added approximately $1 billion to the Americas commercial HVAC backlog. Management expects to convert approximately $500 million of Stellar Energy backlog in 2026, comprising roughly $350 million from the acquisition and $150 million of organic growth, with modest EPS accretion in year one due to high initial investments.

The company’s book-to-bill ratio in Americas commercial HVAC reached approximately 150% in Q1, with backlog up nearly 70% year-over-year. Combined Americas and EMEA commercial HVAC backlog increased by $2.7 billion since year-end 2025, with the Americas up approximately 40%. Importantly, the majority of this backlog consists of applied equipment, which carries a higher-margin services tail that will generate recurring revenue for years to come.

Introduction & Market Context

Trane Technologies plc (NYSE:TT) delivered first-quarter 2026 results that exceeded Wall Street expectations on April 30, 2026, driven by exceptional demand in commercial HVAC markets and record bookings that position the company for sustained growth. The climate solutions provider reported adjusted earnings per share of $2.63, beating analyst forecasts of $2.53 by 3.95%, while revenue of $4.97 billion surpassed expectations by 3.33%.

The company’s stock responded positively to the results and raised full-year guidance, climbing 4.35% in pre-market trading to $485.20, approaching its 52-week high of $501.69. With a market capitalization of $110.6 billion and a P/E ratio of 37.74, Trane Technologies trades at a premium valuation that reflects investor confidence in its growth trajectory, though InvestingPro analysis suggests the stock appears overvalued relative to fundamentals.

Quarterly Performance Highlights

The company’s Q1 2026 presentation revealed a strong operational performance underpinned by record-breaking bookings and backlog growth. As detailed in the following performance overview, Trane Technologies achieved enterprise organic bookings growth of 24% year-over-year, with particularly exceptional strength in the Americas commercial HVAC segment.

The company’s record backlog reached $10.7 billion, representing a 30% increase from year-end 2025 and providing substantial revenue visibility for 2026 and beyond. Americas commercial HVAC bookings surged approximately 40% year-over-year, with applied equipment bookings skyrocketing more than 160%. This exceptional demand was driven by continued strength in data centers and core markets including higher education, government, and healthcare facilities.

Organic revenue growth of 3% year-over-year reflected a mix of flat equipment sales offset by strong low-double-digit services growth. Services now represent approximately one-third of enterprise revenues and have grown at a low-teens compound annual growth rate since 2020, providing a consistent and durable revenue stream.

Included in our AI-picked strategies

·

486.48

▼-6.06(-1.23%)

Closed·01/05·USD

485.00

▼-1.48(-0.30%)

After Hours·19:35:12

Detailed Financial Analysis

The following charts illustrate the company’s solid revenue and earnings per share growth, though margin compression presented challenges in the quarter.

While revenue and EPS grew year-over-year, adjusted EBITDA margin contracted 40 basis points to 17.7% from 18.1% in the prior-year period, and adjusted operating margin declined 20 basis points to 16.0%. Management attributed the margin pressure to inflation, high business reinvestment, and integration costs, which offset volume growth and positive pricing. However, the company’s Business Operating System (BOS) drove operational excellence throughout the P&L, enabling 7% adjusted EPS growth despite the margin headwinds.

Enterprise organic leverage remained strong in the high-teens range, demonstrating the company’s ability to convert revenue growth into earnings even amid cost pressures. The company emphasized its acceleration of incremental business reinvestment across all segments to pull forward high-ROI innovation and growth initiatives.

Segment Performance Analysis

Regional performance varied significantly across Trane Technologies’ three geographic segments, as shown in the following breakdown of bookings and revenues.

The Americas segment delivered exceptional performance with bookings up 29% and revenue up 4% organically. Commercial HVAC bookings and revenues increased approximately 40% and high-single-digits respectively, while services revenue grew at double-digit rates. The residential HVAC business showed mixed results with bookings up low-single-digits but revenues down mid-single-digits. Transport bookings and revenues grew double-digits and low-single-digits respectively, significantly outperforming end markets where truck, trailer, and APU markets declined approximately double-digits.

The following segment margin analysis reveals the operational dynamics across regions.

Americas segment margins remained relatively stable with adjusted EBITDA flat at 19.8% and adjusted operating income up 10 basis points to 17.9%, despite margin deleverage in the residential business due to lower volumes. EMEA faced more significant challenges, with adjusted EBITDA and operating margins both declining 260 basis points to 13.5% and 11.9% respectively, impacted by Middle East headwinds of approximately $25 million in revenue and $0.02 in EPS, along with M&A integration costs. Asia Pacific demonstrated strong margin expansion with adjusted operating income margin up 90 basis points to 22.1%, driven by prudent cost management that offset a challenging China macroeconomic environment.

Strategic Initiatives & Growth Drivers

Trane Technologies’ strategic framework centers on four key pillars designed to deliver differentiated shareholder returns, as illustrated in the company’s focused strategy overview.

The company’s strategy emphasizes winning through sustainable innovation, growing margins and cash via execution excellence, maximizing value as a focused climate company, and continuing dynamic capital allocation. This approach is supported by a strong business operating system, powerful cash flow generation, and an uplifting culture characterized by integrity, ingenuity, and community engagement.

Data center cooling emerged as a particularly significant growth driver in Q1 2026. The company’s acquisition of Stellar Energy, which closed earlier in the year, added approximately $1 billion to the Americas commercial HVAC backlog. Management expects to convert approximately $500 million of Stellar Energy backlog in 2026, comprising roughly $350 million from the acquisition and $150 million of organic growth, with modest EPS accretion in year one due to high initial investments.

The company’s book-to-bill ratio in Americas commercial HVAC reached approximately 150% in Q1, with backlog up nearly 70% year-over-year. Combined Americas and EMEA commercial HVAC backlog increased by $2.7 billion since year-end 2025, with the Americas up approximately 40%. Importantly, the majority of this backlog consists of applied equipment, which carries a higher-margin services tail that will generate recurring revenue for years to come.

Based on the exceptional Q1 performance and record backlog, Trane Technologies raised its full-year 2026 guidance, as detailed in the following comparison.